What Are Results-Based Payments?

Results-based payment is an evolving approach to sustainable development that aims to incentivize climate action, create and expand carbon markets, and stimulate innovation. Through this approach, investors pay an entity – which might be a sovereign nation, a private firm, or a local community – to achieve, report on, and independently verify a set of pre-agreed performance targets. These targets may be tied to the results of climate change mitigation or adaptation activities, such as reducing greenhouse gas emissions, implementing nature-based solutions, or sustainably managing natural resources.

The ER program entities that work on the ground design their own methodology to achieve pre-defined results. This decentralized model allows results-based ER programs to spur creativity and innovation since these stakeholders possess embedded knowledge of the area and the communities therein. Not only are these programs better tailored to the local context, but they are also more agile and better equipped for adaptive management; adaptive management is the process of adjusting program design and implementation according to evolving circumstances or based on lessons learned. Furthermore, these programs also improve accountability and funding effectiveness, because payments are only disbursed after results have been verified. As such, investors can be more certain that their contributions are creating a real impact on the earth.

What’s the Difference Between Climate Finance and Carbon Finance?

The Paris Agreement, an international agreement within the UN Framework Convention on Climate Change (UNFCCC), accounts for both climate and carbon finance. Through this agreement, developed countries resolved to enhance the mobilization and provision of finance, including public and grant-based funds, as well as technology and capacity-building support to enable ambitious climate action. Climate finance transactions, which support climate change mitigation and adaptation activities in developing countries, are accounted for under Article 9 of the agreement.

Transactions under carbon finance, on the other hand, are governed by Article 6 of the Paris Agreement, which provides a centralized accounting mechanism for the international transfer of carbon credits. In a carbon market, countries, as well as non-state actors, can transact emission reduction credits. In essence, the right to pollute becomes tradable, which creates a financial incentive to curb emissions. As emission reduction targets become more ambitious, participating market players are pressured to invest in cleaner technologies and innovate their processes to reduce overall GHG outputs.

How Is Climate/Carbon Finance Disbursed?

An Emission Reductions Purchase Agreement (ERPA) is a legally binding contract between two entities, namely the buyer and seller of ER units, that specifies the terms and conditions for the sale of ERs. The objective of the ERPA is ultimately to incentivize the adoption and expansion of more sustainable land-use practices across entire landscapes and facilitate results-based payments, i.e., the payment of money in exchange for verified ERs. Typically, the terms of an ERPA are agreed during a period of negotiation, during which various issues are discussed, including the anticipated volume of ER units to be generated, the available financing modalities, and the per-unit price of ERs.

How Are ERs Monitored and Verified?

Robust monitoring, reporting, and verification (MRV) is a critical component of the results-based payments approach, as it ensures that ER programs achieve the desired results and enables the distribution of benefits to program stakeholders. ER programs can focus on an entire organization or jurisdiction. ERPAs that are agreed thus facilitate payment for net ERs that are monitored, reported and verified at either the organizational or jurisdictional level.

In most places where ER programs are being implemented, data from the forestry sector is higher quality and easier to obtain compared with data from other sectors, like agriculture and livestock. To incentivize more ambitious emission reductions targets, carbon funds can encourage a comprehensive, multi-sectoral GHG accounting approach. Under this approach, program countries build their capacity to account for emission reductions generated from sectors beyond forestry. As the GHG accounting scope widens, the number of eligible ERs that can be generated increases, so investing in this technical capacity not only augments the amount of available climate and carbon finance but also facilitates the broader transition to low-carbon development.

How Can ER Programs Be Designed Inclusively?

Results-based payments for ERs are oftentimes conditioned upon the development of a comprehensive Benefit Sharing Plan (BSP) which outlines how monetary and non-monetary benefits will be distributed to program stakeholders. Inclusive, accessible, and transparent stakeholder consultations are essential when designing these plans, because they help the ER program secure buy-in from local communities and understand their preferences; the process also ensures that there is two-way communication about how and when communities can receive benefits. During the consultation process, stakeholders are made aware that the distribution of benefits relies on the successful generation, verification, and transfer of ERs. Any potential risks to ER generation and transfer should be clearly communicated, in case the ER program underperforms or does not perform. Safeguard mechanisms should also be put in place in order to address potential environmental and social risks, in order to avoid (or mitigate) possible harms. Safeguards plans are typically required before an ERPA is signed.

How Can ER Programs Mitigate Risk?

In order to account for risks related to uncertainty and reversals, certain ER units, called “buffer ERs,” can be set aside in an ER transaction registry and deducted from the total volume of verified ERs generated by a program entity. This means that a share of the ERs generated are held in reserve in case any future events reverse the ERs that were generated.

- Uncertainty buffer ERs are verified ERs that are reserved in the transaction registry to account for the level of uncertainty associated with the estimation of emission reductions. These buffer ERs may account for errors related to estimating emissions baselines or measuring emission reductions.

- Reversal buffer ERs are verified ERs that create a buffer for the ER program’s level of reversal risk. ER reversal is the intentional or unintentional release of carbon back into the atmosphere; a reversal might be caused by natural disturbances, climate change, and/or anthropogenic activities. For example, if an ER program generates 10 million tons of ERs over a five-year period, but in the fifth year a forest fire occurs which generates one million tons of GHG emissions, the previously transacted and paid for ERs are protected against this reversal event by the cancelation of one million reversal buffer ERs.

Once ERs are verified and buffer ERs are set aside, the remaining ERs are available to be transacted under the ERPA.

How Are Results-Based Payments Governed Under the ISFL?

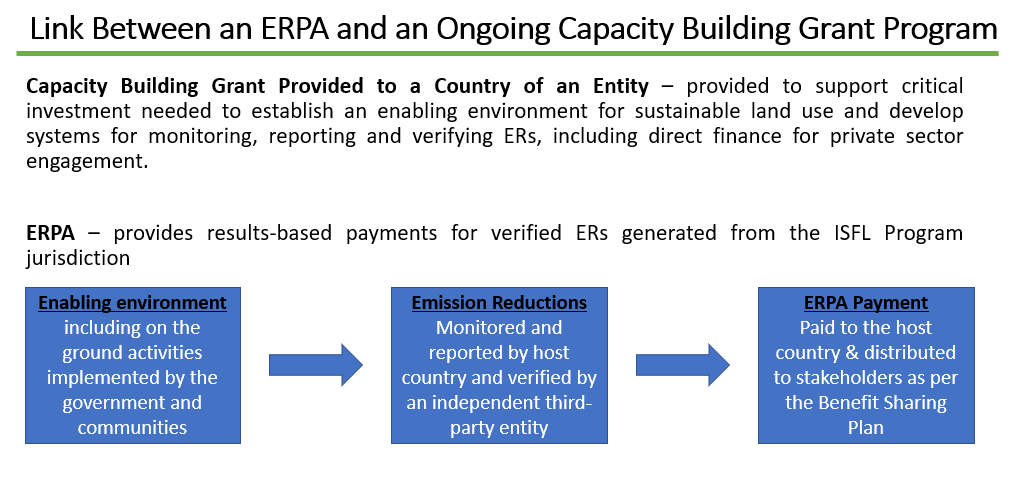

The BioCarbon Fund Initiative for Sustainable Forest Landscapes (ISFL) is a multilateral fund, supported by donor governments and managed by the World Bank, that works to reduce greenhouse gas (GHG) emissions from the land sector. The fund enables program countries to implement integrated land-use planning at scale through a two-pronged approach. First, the ISFL provides up-front grant financing and technical support to program countries, which enable them to improve jurisdictional land-use management. Then, the fund provides monetary payments in exchange for results, which take the form of verified emission reductions (ERs). This model incentivizes a broad range of actors within the public sector, private sector, and local communities to adopt sustainable practices on the ground. ISFL pilot programs are currently being implemented in five countries: Colombia, Ethiopia, Indonesia, Mexico, and Zambia.

Up until now, the ISFL has been primarily focused on mobilizing grant financing to create an enabling environment for sustainable land use. Going forward, the five ISFL program countries are preparing to secure results-based payments through Emission Reductions Purchase Agreements (ERPAs), which at the simplest level are contracts which make payments to countries for reducing emissions. By effectively implementing landscape-level sustainable land-use programs, ISFL program countries can expect to generate a substantial volume of ERs that are eligible for remuneration once they have been recorded and verified. This article lays out the processes involved when securing payment for ERs.

Financing Modalities Under the ISFL

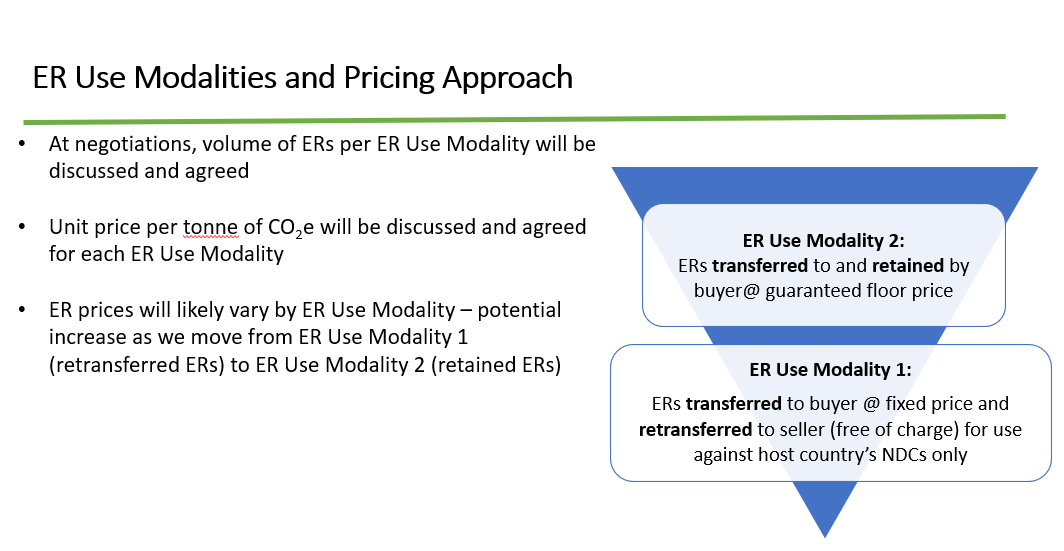

The ISFL provides program countries with both climate finance and carbon finance. Under a climate finance modality, also called ER Use Modality 1 by the fund, the ISFL makes payments for verified ERs but does not retain ownership of these ERs. This means that, after being sold to the World Bank, the ER unit is transferred back to the ISFL program country for use towards its nationally determined contributions (NDCs) under the Paris Agreement. For ERs purchased by the ISFL under a carbon finance modality, however, the ISFL will make payments for verified ERs but will not transfer them back to the ISFL program country, but rather forward them to the donor country who retains ownership of the verified ERs. As such, ISFL program countries selling ERs under a carbon finance modality, also called ER Use Modality 2, will not be able to use these ERs to fulfill their NDCs, which creates an opportunity cost. Under this modality, program countries must find other climate mitigation opportunities to meet their emission reduction goals, so they may demand a higher price for ERs.

Regardless of the ER use modality being used, there is a consistent need to ensure the robustness of the verified ERs. For transactions under both climate and carbon finance, ER units must first be verified by a third party to ensure that they have met the necessary standards. Under the ISFL, the verification standard that is used is provided by the ISFL ER Program Requirements, a public document outlining the ISFL’s methodology for ER transactions.

Furthermore, the seller of ERs must demonstrate an ability to transfer the title of those ERs to the buyer (e.g., through ER ownership or transfer authorization) and the right to sell the ERs generated. This can be achieved in a variety of ways, including referencing the appropriate legislation or even issuing new legislation if there is currently none.

ISFL ERPAs

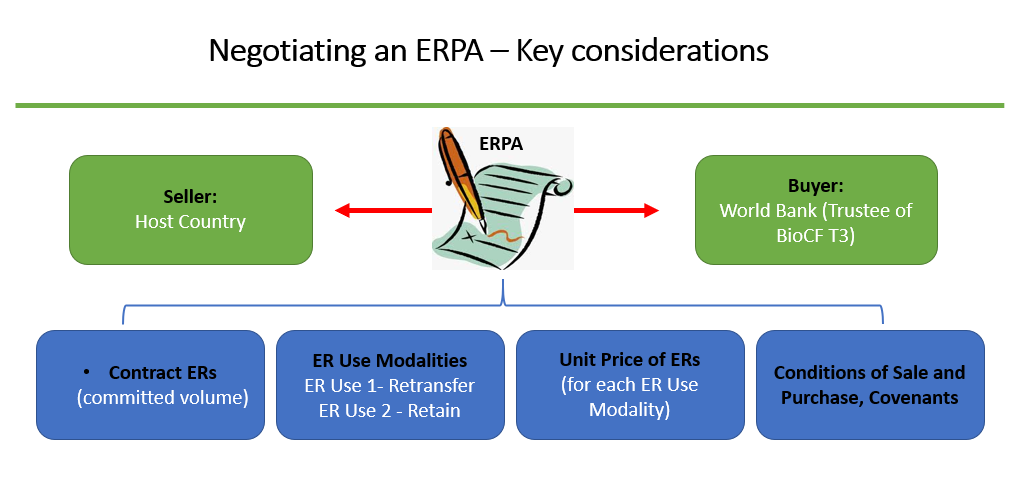

An Emission Reductions Purchase Agreement (ERPA) is a legally binding contract between two entities, namely the buyer and seller of ER units. Under the ISFL, the two entities are the World Bank, which is the buyer as trustee of the BioCF Tranche 3 (T3),[1] and the government of an ISFL program country, the seller, which implements an emission reductions program to generate units for sale. The ERPA specifies the terms and conditions for the sale of ERs. The objective of the ERPA is ultimately to incentivize the adoption and expansion of more sustainable land-use practices across entire landscapes and facilitate results-based payments, i.e., the payment of money in exchange for verified ERs that conform to the ISFL’s methodological requirements. The terms of an ERPA are agreed during a period of negotiation, during which various issues are discussed, including the data contained within the country’s ERPD and the anticipated volume of ER units to be generated.

To summarize, the key commercial terms of an ISFL ERPA include:

- The volume of ERs to be transacted: The number of ER units are contracted in metric tons, and, in most situations, volumes range between 5 and 15 million metric tons of CO2. The contracted ER volume is based upon the best possible estimate for the volume of ERs to be generated within a specific jurisdiction and time period by an ISFL ER program. Should the volume of ERs that is generated under the ER program be less than the contracted ER volume, the amount of results-based payments would be reduced accordingly.

- The ER use modalities: The ISFL purchases ERs based on two distinct ER use modalities. ER Use Modality 1 relates to ER units which are purchased by the ISFL but subsequently returned to the ISFL program country for use toward its nationally determined contributions (NDCs) under the Paris Agreement. This modality is funded by BioCF T3 and reported as climate finance under Article 9 of the Paris Agreement. ER Use Modality 2 relates to ER units which are purchased by the ISFL and retained by the relevant BioCF T3 participants. The ISFL program country selling the ERs loses title to these ER units and is no longer able to use these ER units towards its NDC.

- The unit price for ERs: The per unit price of ERs is determined in US dollars. Prices may differ, depending on the results of negotiations and between ER use modalities. An ISFL program country will likely expect a higher price for ER units governed under ER Use Modality 2, as use of this modality is accompanied by a significant opportunity cost to the country; it cannot use the ERs it generates to fulfill its NDCs since ownership is retained by ISFL donors.

- Conditions of sale, purchase, and covenants: Four major technical specifications must be discussed during the ERPA negotiation process: the monitoring, verification, and reporting (MRV) system, compliance with ISFL ER Program Requirements, the development of a benefit sharing plan (BSP), and the design of safeguards mechanisms. Each of these will now be discussed in turn.

Technical Specifications

- Monitoring, reporting, and verification (MRV) of ERs: The ISFL ER Program Requirements specify the requirements relating to the monitoring, reporting, and verification of ER units. As ER units are complex assets that cannot be physically examined, it is critical that a clear and transparent auditing process is designed to ensure that the ERs being sold have indeed been generated, and that the GHG emissions within the jurisdiction have been reduced when compared to a baseline reference level. This rigorous process, which is laid out and mutually agreed by all parties in the ERPA, ensures that the buyer of an ER unit can be confident in the quality of the ER they are purchasing.

- Compliance with ISFL ER Program Requirements: The ISFL ER Program Requirements outline the standard that the ISFL uses to define an ER unit. It is a public document that explains how baselines are set and how emission reductions are calculated. All ERs purchased under an ISFL ERPA must comply with these requirements, and ER programs must provide proof of compliance through an Emission Reductions Program Document (ERPD), so that the quality of the ER units can be standardized across the fund. The ERPD provides information on the estimated emission reductions and removals expected for a given ERPA phase, as well as the emissions baseline, anticipated interventions, financing plan, and GHG accounting scope and improvement plan. The ERPD, therefore, encompasses all the technical and organizational aspects of the ISFL ER program. The ERPD is validated by an independent third party – a validation and verification body (VVB) – after which donors participating in BioCF T3 provide their input and approval to move forward with ERPA negotiations.

- Development of a benefit sharing plan (BSP): The ISFL will only disburse payments for ERs when a ISFL program country has published a final benefit sharing plan which outlines how results-based payments as well as non-monetary benefits will be distributed to ISFL ER program stakeholders. When developing BSPs, stakeholder consultations are essential because they help the program to secure buy-in from local communities and understand their preferences; the process also ensures that there is two-way communication about how and when communities can receive benefits. During the consultation process, stakeholders are made aware that the funds under the BioCF ISFL are results-based financing vehicles, which means that benefit sharing relies on the successful generation, verification, and transfer of ERs. Any potential risks to ER generation and transfer should be clearly communicated, in case the ISFL ER program underperforms or does not perform. This document will be submitted for the World Bank and participants in BioCF T3 for their review before it is published. More information on benefit sharing plans can be found in the Note on Benefit Sharing for Emission Reductions Programs and Designing Benefit Sharing Arrangements: A Resource for Countries.

- Design of safeguards mechanisms: All ISFL ER programs must be implemented in accordance with World Bank safeguards requirements (specifically the World Bank’s Environmental and Social Framework). These requirements ensure that ISFL program countries implement emission reductions activities in a way that addresses potential environmental and social risks, in order to avoid (or mitigate) possible harms. Safeguards plans are typically required before an ERPA is signed.

Monitoring, Reporting, and Verification

Robust monitoring, reporting, and verification (MRV) is a critical component of results-based payments, as it ensures that ER programs achieve the desired results and enables the distribution of benefits to program stakeholders. Each ISFL ER program focuses on an entire jurisdiction – on a state, province, or region – so ERPAs under the ISFL facilitate payment for net emissions reductions that are monitored, reported, and verified at the jurisdictional level.

For most ISFL program countries, data from the forestry sector is higher quality and easier to obtain compared with data from other sectors, like agriculture and livestock. Because the ISFL adopts a comprehensive, multi-sectoral GHG accounting approach, program countries are incentivized to build capacity to account for emission reductions generated from sectors beyond forestry. Overall, investing in technical capacity building facilitates the transition to low-carbon development by augmenting the amount of available climate and carbon finance; as the GHG accounting scope widens, the number of eligible ERs that can be generated increases.

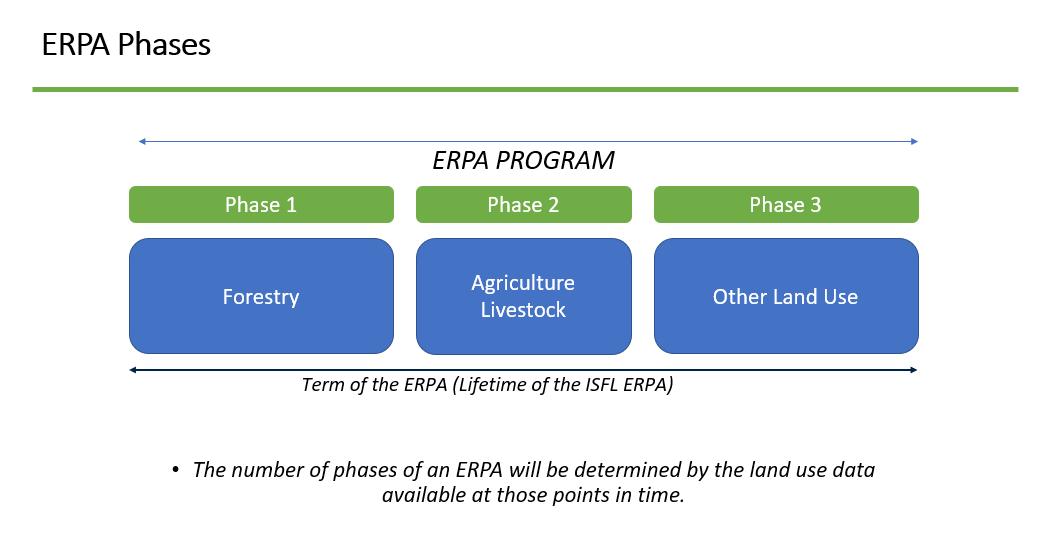

Continued technical capacity building for GHG accounting enables countries to raise the ambition of their emission reductions targets. ISFL ERPAs are phased, which means that they are designed so that program countries can increase the accounting scope of their ISFL ER program stepwise over time and be paid for additional verified ERs as they add more sectors. An ISFL program country may sign an ERPA committed to deliver ERs from one sector (e.g., forests) during the first ERPA phase, which might cover a time period of a few years, and, as additional sectors are added, the country will negotiate and sign additional ERPAs that would enable the delivery of ERs generated from additional sectors (e.g., agriculture and/or livestock) during subsequent phases. For each ERPA phase, ERs are measured against an emissions baseline, which refers to the level of emissions recorded in the jurisdiction at a specific point in time before ISFL ER program implementation began.

During an ERPA phase, the generation of ERs under the ISFL ER program may be verified once or multiple times by a VVB, depending on the stipulations laid out in the ERPA for each phase. VVBs must verify ERs and produce a verification report before ERs are issued into an emission reductions transaction registry. To prepare for the verification process, the ISFL program country monitors and reports on the ERs generated using an ER Monitoring Report template.

The ER Monitoring Report should include technical information (i.e., the volume of ERs generated) as well as information on safeguards, BSP implementation, and ER title transfer. For instance, for the first verification of a potential ERPA payment, an ISFL ER program would report on the readiness of benefit-sharing arrangements, and during subsequent verifications, it would provide progress updates on the implementation of those arrangements. Similarly, for safeguards, an ISFL program country would report on its compliance with the World Bank safeguards requirements.

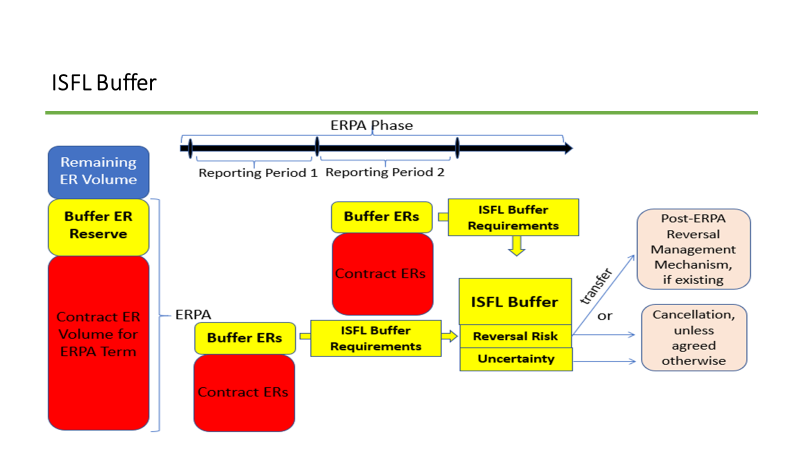

Explaining Buffers and ER Issuance

Most ISFL program countries have not yet created their own national ER registries. This raises a significant challenge to accessing climate and carbon finance, because a mechanism that enables ER units to be issued and transacted in a robust and transparent way is necessary. ER issuance is the process by which a registry administrator “issues” a specified quantity of verified ERs for a project activity into a pending account in the registry. To overcome this hurdle, the World Bank has developed an ER transaction registry for use by ISFL program countries and BioCF T3 participants. This registry is known as the Carbon Assets Tracking System (CATS). CATS supports the issuance and transaction of verified ER units generated under the ER programs of World Bank-administered climate initiatives, including the ISFL.

In order to account for risks related to uncertainty and reversals, certain ER units, called “buffer ERs,” are set aside in CATS and deducted from the total volume of verified ERs, as per the ISFL Buffer Requirements. This means that a share of the ERs generated are held in reserve in case any future events reverse the ERs generated within a jurisdiction. The ISFL has two specific types of buffers designed to mitigate two distinct risks.

- Uncertainty buffer ERs are verified ERs that are reserved in the transaction registry to account for the level of uncertainty associated with the estimation of emission reductions during a given ERPA phase. These buffer ERs may account for errors related to estimating emissions baselines or measuring emission reductions.

- Reversal buffer ERs are verified ERs that create a buffer for the ER program’s level of reversal risk. ER reversal is the intentional or unintentional release of carbon back into the atmosphere; a reversal might be caused by natural disturbances, climate change, and/or anthropogenic activities. For example, if an ISFL program country generates 10 million tons of ERs over a five-year period, but in the fifth year a forest fire occurs which generates one million tons of GHG emissions, the previously transacted and paid for ERs are protected against this reversal event by the cancelation of one million reversal buffer ERs.

Once ERs are verified and buffer ERs are set aside, the remaining ERs are available to be transacted under the ERPA. Payments received by the ISFL program country for these ERs are then distributed to eligible beneficiaries as per the BSP.

Current State of ISFL ERPAs

All five ISFL country programs are making good progress towards ERPA negotiations. The chart below illustrates when ERPDs are expected to be received by the ISFL, when ERPA negotiations are expected to commence and when ERPAs are anticipated to be signed. The first ERPA signature is expected to occur later in 2021 with subsequent ERPAs anticipated in 2022 and 2023. These ERPAs are expected to run until 2030.

Key Terms for Understanding How Results-Based Payments Work Under the ISFL

ERPD: To be able to negotiate and sign an ERPA with the ISFL, an ISFL program country needs to demonstrate that its ER program conforms with the ISFL ER Program Requirements (the methodology for carbon accounting that the ISFL follows). In order to demonstrate compliance, the country program prepares an Emission Reductions Program Document (ERPD). The ERPD is a comprehensive document which provides information on the technical and organizational aspects of the ER program. In addition, the ERPD lays out a plan of action for generating ERs, including implementation activities that will result in improved sustainability. ERPDs also provide information on the GHG baseline for the jurisdiction; calculating this baseline accurately is critical as it is the reference level by which all future ER verifications will be compared against.

BSP: Prior to signing an ERPA, an ISFL ER program country needs to submit a Benefit Sharing Plan (BSP). The BSP details how the funds generated by the sale of ERs under an ERPA will be shared among ISFL ER program stakeholders. BSPs are an integral part of each ER program and seek to ensure that the payments for ERs flow to the actors on-the-ground that have played a role in generating them. In many cases, the beneficiaries will be individuals and communities who live and work in the jurisdiction, and who adopt sustainable practices that generate ERs. A BSP is invaluable to all stakeholders: donors and investors are assured that their payments for ERs are sponsoring real emission reductions; program countries can demonstrate that ER sales are directly benefiting their core constituencies; and stakeholders who are working to generate ERs know their efforts will be rewarded with concrete improvements to their livelihoods.

ERPA: Through the ISFL, results-based payments are facilitated through Emission Reductions Purchase Agreements (ERPAs) and are aimed toward enabling and scaling up improved forest management and sustainable land-use practices across jurisdictional landscapes. An ERPA is a contract between two entities – the buyer and the seller of the ERs. For the ISFL, Tranche 3 of the BioCF (BioCF T3) is the buyer of the ERs while the ISFL ER program country is the seller of the ERs. ERPAs detail delivery dates, quality specifications, volumes, and pricing, which are typical of general contracts. Furthermore, because the intricacies of ER transactions require additional technical specificities, the ERPA also includes information on the ER use modality, the specific timing and rigor of the verification process -- including the underlying carbon accounting methodologies to be used -- and additional obligations relating to reporting for the UNFCCC. For the ISFL, most ERPAs will likely contain a combination of ER use modalities with different prices for each modality. Bearing in mind the complexity and uniqueness of ISFL ERPAs, the World Bank legal department in collaboration with the ISFL Fund Management Team will provide ISFL program countries with training on ERPAs prior to entering the negotiation process.

NDC: A Nationally Determined Contribution is a plan by a party to the Paris Agreement to take climate action through emission reduction targets and policies, adaptation plans, and other climate action goals. New plans should be proposed every five years that increase the ambition of the original goals.

[1] The ISFL has two key funding instruments, BioCFplus ISFL and BioCF T3, which have been designed specifically to operationalize the vision of the ISFL. BioCFplus ISFL supports grant-based technical assistance and capacity-building efforts in each jurisdiction. It provides the critical investment finance needed to establish an enabling environment for sustainable land-use and develop systems for monitoring, reporting, and verifying GHG emission reductions. In addition, BioCFplus ISFL directly finances advisory service projects aimed at attracting private sector interest in ISFL jurisdictions, which can benefit farmers as well as other actors (see Appendix B for details on donor contributions and cumulative expenses). BioCF T3 provides results-based payments for verified reductions in GHG emissions through an Emission Reductions Purchase Agreement. The BioCFplus ISFL, in combination with results-based finance from BioCF T3, allows ISFL programs to use context-specific tools and approaches to reduce emissions from land-use sectors.